Table Of Content

These taxes generally pay for services such as road repairs and maintenance, school district budgets and county general services. This is based on our recommendation that your total monthly spend for your monthly payment and other debts should not exceed 36% of your monthly income. A down payment of 20% or more will get you the best interest rates and the most loan options. There are a variety of low-down-payment options available for home buyers.

Calculate your mortgage payments

This can help you decide whether to prepay your mortgage and by how much. In addition to mortgages options (loan types), consider some of these program differences and mortgage terminology. A HELOC is a line of credit that lets you borrow against the equity in your home. It works similarly to a credit card in that you borrow what you need rather than getting the full amount you're borrowing in a lump sum.

What are origination fees?

It's important to understand how your interest rate, down payment, property location, term and other factors can affect your mortgage payment. Find out how to use a home loan calculator and see how this tool can make calculating your estimated mortgage payment easier. In most cases, the amortized payments are fixed monthly payments spread evenly throughout the loan term. Each payment is composed of two parts, interest and principal. Interest is the fee for borrowing the money, usually a percentage of the outstanding loan balance.

How does the Federal Reserve affect mortgage rates?

It also lets you tap into the money you have in your home without replacing your entire mortgage, like you'd do with a cash-out refinance. With Chase for Business you’ll receive guidance from a team of business professionals who specialize in helping improve cash flow, providing credit solutions, and managing payroll. Choose from business checking, business credit cards, merchant services or visit our business resource center.

Should I choose a long or short loan term?

A fixed rate is when your interest rate remains the same for your entire loan term. An adjustable rate stays the same for a predetermined length of time and then resets to a new interest rate on scheduled intervals. A 5-year ARM, for instance, offers a fixed interest rate for 5 years and then adjusts each year for the remaining length of the loan.

Get pre-qualified

Like homeowners insurance, property taxes can vary significantly depending on where you live. You’ll likely have the option of paying your property taxes from an escrow account. The Rocket Mortgage calculator takes those taxes into consideration when giving you an estimated monthly mortgage payment. The answer depends on several factors including your interest rate, your down payment amount and how much of your income you’re comfortable putting toward your housing costs each month. Assuming an interest rate of 6.9% and a down payment under 20%, you’d need to earn a minimum of $150,000 a year to qualify for a $400,000 mortgage.

Property taxes

A low DTI demonstrates that you have a good balance between debt and income, while a high DTI signals that your debt may be too high for your income. If you opt for ARMs, your mortgage interest rates (and monthly payment) will change over time. Some of the recurring expenses will change over the lifetime of home ownership due to home value changes, inflation and other factors. Some expenses (e.g., property taxes, homeowner's insurance etc.) will continue even after you have paid off your loan. You should consider all these factors, especially when making a rent vs. buy decision.

You may be surprised to see how much you can save in interest by getting a 15-year fixed-rate mortgage. Use our mortgage calculator to get an idea of your monthly payment by adjusting the interest rate, down payment, home price and more. To find out how you can pay off your mortgage faster, try our mortgage payoff calculator. The larger your down payment, the more likely you are to qualify for lower interest rates. We recommend your down payment be at least 5% of the purchase price. Whether you’ll need to pay for mortgage insurance will depend on the type of loan you get and the size of your down payment.

Confirm your affordability with multiple lenders

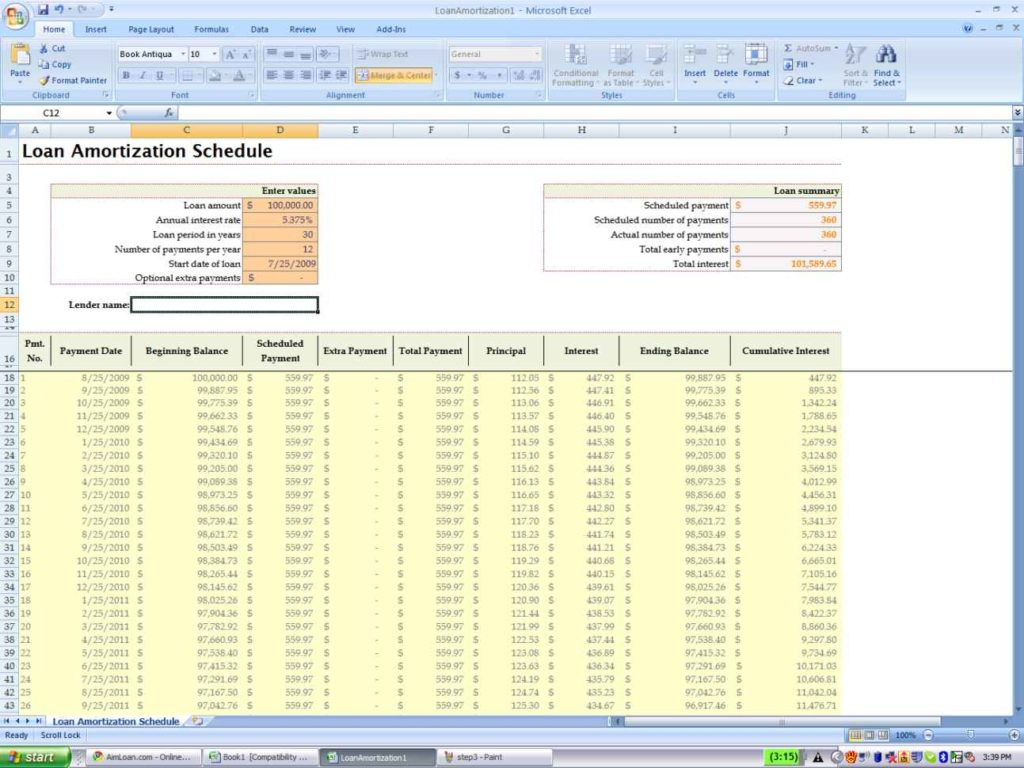

Your credit score is one factor used to determine which loan products you might qualify for. Most lenders offer you options based on your credit score and other factors like your monthly income and your debts. If you have a credit score of 740 or above, you may qualify for a lower interest rate. The Mortgage Amortization Calculator provides an annual or monthly amortization schedule of a mortgage loan. It also calculates the monthly payment amount and determines the portion of one's payment going to interest. Having such knowledge gives the borrower a better idea of how each payment affects a loan.

Georgia Mortgage Calculator - The Motley Fool

Georgia Mortgage Calculator.

Posted: Thu, 07 Mar 2024 08:00:00 GMT [source]

It also allows the lender to take the house if you don’t repay the money you’ve borrowed. Lenders typically require you to purchase homeowners insurance when you have a mortgage. The coverage you’re required to purchase may vary by location. For example, if you live in a flood zone or a state that’s regularly impacted by hurricanes, you may be required to buy additional coverage that protects your home in the event of a flood. If you live near a forest area, additional hazard insurance may be required to protect against wildfires. This is the amount you borrow from your lender to buy your home.

If you’re new to homeownership, you may not realize that the loan amount isn’t the only factor to consider when determining how to calculate a mortgage payment. Let’s look at how mortgage payment calculators break down your monthly mortgage expenses. Assuming you've made a 20% down payment on a $500,000 home and a 30-year, $400,000 mortgage at 7.2% would require a monthly payment of about $2,715. You'd need to show a lender you can afford to make that payment and meet your other financial obligations. Most lenders want to ensure your mortgage payment is less than one-third of your monthly income. An obvious but still important route to a lower monthly payment is to buy a more affordable home.

Minnesota Mortgage Calculator - The Motley Fool

Minnesota Mortgage Calculator.

Posted: Thu, 07 Mar 2024 08:00:00 GMT [source]

An ARM, or adjustable rate mortgage, has an interest rate that will change after an initial fixed-rate period. In general, following the introductory period, an ARM’s interest rate will change once a year. Depending on the economic climate, your rate can increase or decrease. You have many options when it comes to choosing a mortgage lender.

Determining what your monthly house payment will be is an important part of figuring out how much house you can afford. That monthly payment is likely to be the biggest part of your cost of living. The longer the term of your loan — say 30 years instead of 15 — the lower your monthly payment but the more interest you’ll pay. Sky high mortgage rates have pushed many hopeful buyers out of the market, slowing homebuying demand and putting downward pressure on home prices.

That leaves plenty of room in your budget to achieve other goals, like saving for retirement or putting money aside for your kid’s college fund. The interest rate does not change for the first five years of the loan. After that time period, however, it adjusts annually based on market trends until the loan is paid off. The interest rates are usually comparable to a 30-year mortgage, but ARMs transfer the risk of rising interest rates to you—the homeowner. A quick conversation with your lender about your income, assets and down payment is all it takes to get prequalified.

This allows you to better compare different types of mortgages from different lenders, to see which is the right one for you. A 30-year mortgage will have the lowest monthly payment amount but usually carries the highest interest rate—which means you’ll pay much more over the life of the loan. Before you lock in an interest rate, it’s worth knowing that high interest rates bring higher monthly payments and increase the amount of interest you’ll pay over the life of your loan.

No comments:

Post a Comment