Table of Content

On the other hand, conventional mortgages have a lower back-end DTI limit, which is usually 36%. But depending on the strength of your credit history, it can stretch up to 43%. Other conventional lenders may allow up to 50% with compensating factors. When homeowners could not afford to pay the large balloon payment, they kept on refinancing their mortgage to extend the term. Eventually, many borrowers could not afford the costly balloon payments, which resulted in massive foreclosures.

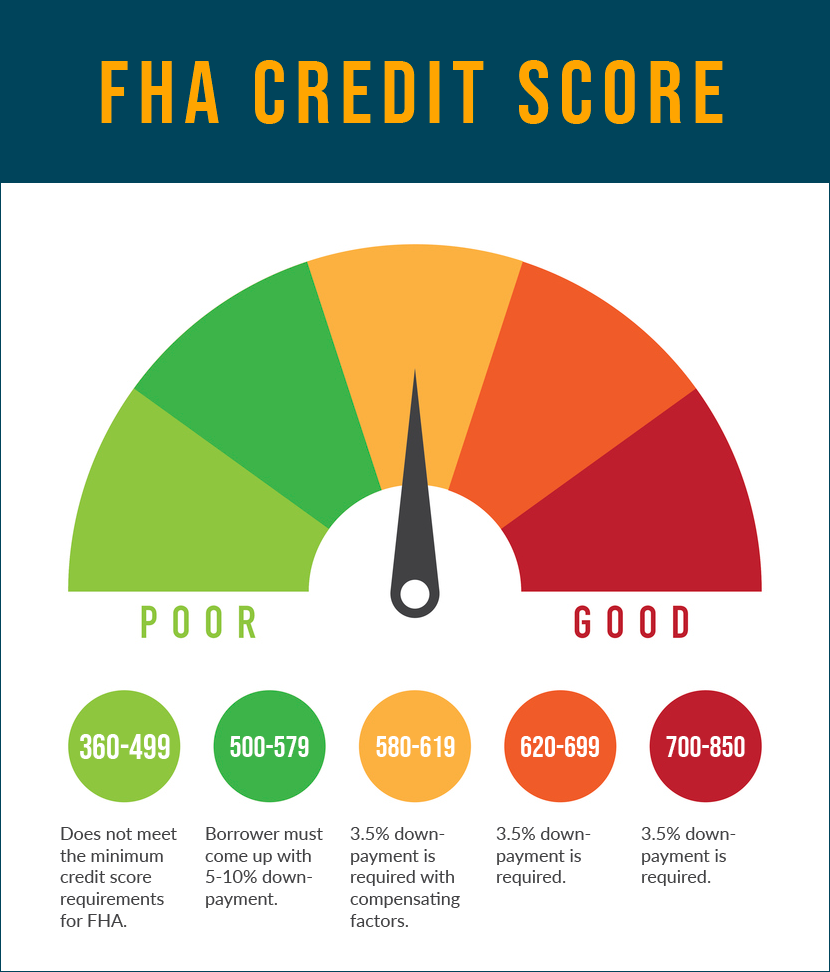

If your credit score falls at 620 and below, it’s harder to obtain a conventional loan. With conventional mortgages, the higher your credit score, the lower the rate you’ll receive. Meanwhile, if you have a low credit score, you’re bound to receive a much higher rate with a conventional loan. In other cases, a conventional lender might not approve your application at all. Private Mortgage Insurance is calculated based on your credit score and amount of down payment. If your loan amount is greater than 80% of the home purchase price, lenders require insurance on their investment.

Mortgage and refinance rates today, Dec. 24, and rate forecast for next week

This is only required if you offer less than 20% down payment. It is also automatically canceled once you’ve gained sufficient equity on your home. Throughout the decades, the FHA program has made mortgages accessible to many homebuyers. Today, qualified FHA borrowers are guaranteed 96.5% financing.

Risk-free rate of return itself is composed of two components. The first is expected inflation and the second is time preference for money. An investor does not want to lose their savings to inflation and so they factor their inflation expectations into their expected rate of return.

What is FHA Mortgage Insurance and How Much Does It Cost?

The FHA also determines your eligibility criteria to apply for an FHA loan. Press escape to close or press tab to navigate to available options. This link takes you to an external website or app, which may have different privacy and security policies than U.S. We don't own or control the products, services or content found there.

Borrowers with a 30-year fixed-rate jumbo mortgage with today’s interest rate of 6.65% will pay $642 per month in principal and interest per $100,000. That means that on a $750,000 loan, the monthly principal and interest payment would be around $4,825, and you’d pay approximately $983,305 in total interest over the life of the loan. At today’s interest rate of 5.77%, a 15-year fixed-rate mortgage would cost approximately $831 per month in principal and interest per $100,000.

Do FHA interest rates vary by lender?

Borrowers may be able to save on interest costs by going with a 15-year fixed mortgage, as they generally have a lower rate than that of a 30-year, fixed-rate home loan. But keep in mind that you’ll have higher monthly payments since you’re paying off your loan in half the time . The terms available through FHA loan programs can be attractive to borrowers who wouldn’t otherwise be able to afford large down payments or even qualify for conventional mortgages. FHA loans are also beneficial for those who have weak or damaged credit. Some FHA mortgage lenders allow credit scores as low as 500, though a higher score will decrease your down payment requirement. If you’ve had financial difficulties in the past or you just haven’t had time to build a strong history of on-time payments, an FHA loan could be the answer to your mortgage needs.

If you're looking to buy a house, keep in mind that the Fed has signaled it will continue to raise rates into 2023, which would likely continue to drive mortgage rates upward. A few notable mortgage rates dropped off over the last seven days. The average interest rates for both 15-year fixed and 30-year fixed mortgages tumbled more than a 10th of a percentage point. We also saw a shrinking in the average rate of 5/1 adjustable-rate mortgages. Major mortgage rates ticked downward this week, though rates remain high compared to earlier this year.

FHA LOAN LIMITS

This has pushed some homebuyers out of the market and cooled the housing prices in some areas. But while the overall market remains this expensive, homebuyers should welcome every bit of help they can get. Mortgage lenders will preapprove you for a loan based on your income, credit score, assets, and other considerations. If you're eligible for both an FHA loan and a conventional loan, then you'll want to compare the mortgage rate and fees for each loan type. Conforming loan limits also establish which loans can be purchased by Fannie Mae or Freddie Mac on the secondary mortgage market. Because lenders can more easily sell conforming loans, they tend to make these loans more affordable for borrowers .

The buyer might be a government agency or it might be a government-sponsored enterprise , like Fannie Mae and Freddie Mac, or it might even be a private entity. These buyers combine pools of mortgages and use them as collateral on bonds that they issue. In effect, they turn pools of mortgages into mortgage-backed securities . Through the MBS medium, your mortgage obligation and the lien on your house are traded regularly on the secondary market. FHA rates are determined based on the rates of securities composed of FHA mortgages. Supply and demand determine the rates of mortgage-backed securities in the free market.

An FHA loan may be your only option if you do not meet the credit qualifications of a conventional loan. A conventional mortgage is a better option if your credit score is above 740. If this is your circumstance, then you do not need to pay for the expensive mortgage insurance required for FHA loans. However, mortgage insurance may still apply to conventional loans when the down payment is less than 20%. This means that depending on your lender, FHA rates may be higher or lower than prevailing conventional loan rates.

Around the early 2000s, these lenders began offering conventional mortgages to high-risk borrowers with weak credit backgrounds. Some conventional loan programs even offered zero down payment options (100% financing), and mortgages with extended 40 and 50-year payment terms. Refinance your existing mortgage to lower your monthly payments, pay off your loan sooner, or access cash for a large purchase. Use our home value estimator to estimate the current value of your home. See our current refinance ratesand compare refinance options.

However, credit will have less of an impact on FHA mortgage rates than it does on conventional loan rates. All Loan Estimates use the same format so you can easily compare them side by side. Moreover, section 251 allows borrowers to take FHA loans as adjustable-rate mortgages .

Today, the department continues to help make homebuying accessible to more Americans. FHA programs are known for low down payment options and relaxed credit qualifications. After the global COVID-19 health and economic crisis mortgage rates reached all time record lows in October 2020.

Borrowers who have a low credit score or can't afford a large down payment may want to consider an FHA loan. Backed by the Federal Housing Administration, these mortgages have a lower minimum down payment and more lenient credit requirements. This is regardless of the borrower's credit score and down payment. Your total mortgage payment must be below 31% of your gross monthly income. Mortgage payments include property taxes, mortgage insurance, homeowners insurance and homeowners association fees . Adjustable-rate mortgages pretty much always have lower initial mortgage rates than fixed-rate loans.

While it’s a large sum, it will help you bypass private mortgage insurance . On the other hand, many homebuyers offer less than 20% down, which requires them to pay PMI for a limited time. Once your loan-to-value ratio reaches 78%, PMI is automatically removed on a conventional mortgage. As the economy continued to grow, many mortgage lenders became brash and overly confident about extending credit.

No comments:

Post a Comment